In [1]:

%load_ext autoreload

%autoreload 2

import numpy as np

import matplotlib.pyplot as plt

from quantfinlib.sim import BrownianMotion

Random walk

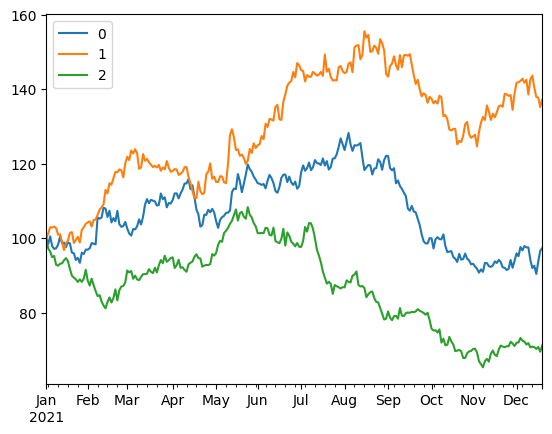

Below a plot of 3 scenarios of Brownian Motion (BM) random walk, \(dS = \mu + \sigma dW\)

In [2]:

gbm_sample(

s0=120.70,

vol=0.25,

drift=0.02,

t0='2021-01-01',

freq='B',

path_len=252,

num_paths=3

).plot()

plt.show()